The global transition to a low-carbon economy is creating a new breed of mid- and large-cap companies in the Resources & Energy sectors. Unlike the 2000-2014 resources supercycle, which was principally driven by demand for bulk commodities (i.e., iron ore and coal), demand is currently surging in clean-energy commodities such as lithium, the rare earth elements, nickel, copper and uranium. Because these commodities are not the primary source of revenue of most of the big Resources & Energy companies, a new breed of mid- and large-cap companies is appearing on the ASX. These newcomers are disrupting the compositional mix of Resources & Energy companies on the ASX. Therefore, it is not the household names of old that are driving growth in the Resources & Energy sectors but a new bunch of companies with names and commodities that most investors are unfamiliar with.

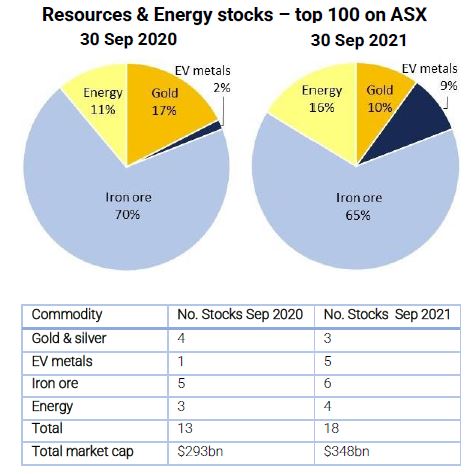

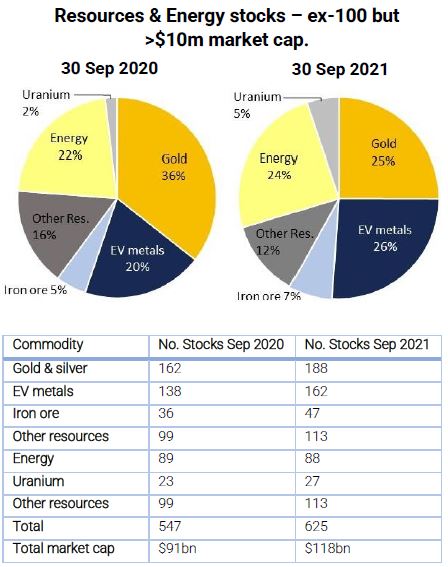

To highlight the impact of the clean energy transition on the Resources & Energy sectors we produced pie charts that compare the differences in commodity mix between 30 September 2020 and 30 September 2021. The two top charts are for Resources & Energy stocks in the top 100 of the ASX and the lower two charts are for stocks outside the top 100 but with a market capitalisation >$10m (i.e., the main investment universe of the NextGen Resources Fund). The sectors are grouped according to the principal source of revenue (or value, for explorers and developers) based on market capitalisation.

For Resources & Energy stocks in the top 100 of the ASX, the most striking feature of the compositional mix is the dominance of iron ore exposure. In the last 12 months iron ore exposure has declined from 70% to 65%, but still represents about 2/3 of the universe. This means anyone who only invests in Resources & Energy stocks in the top 100 on the ASX is heavily exposed to commodities from the old resources supercycle (i.e., iron ore and coal). Despite this decline, the total market cap for the top 100 Resources & Energy stocks grew in the last 12 months from about $293bn to $348bn. The main contributor to this growth were companies predominantly exposed to the clean energy commodities (i.e., EV metals), which increased from about 2% to 9%. However, this growth was driven by 4 new stocks that entered the top 100 of the ASX. In September 2020, copper producer Oz Minerals was the only company in this sector, but 12 months later it was joined by rare-earths producer Lynas and lithium-exposed companies IGO, Pilbara and Orocobre. Investors in the NextGen Resources Fund will recognise Lynas, Pilbara and Orocobre as 3 of the fund’s strong performers over the last 12 months. Therefore, clean energy commodities are a rapidly growing sector in the top 100 of the ASX, but the growth is coming from mid-cap companies entering the large-cap universe.

For Resources & Energy stocks outside the top 100 on the ASX but with market caps >$10m, major disruptions also occurred to the commodity mix. The decline in exposure of the gold sectors, which is also evident for top-100 stocks, was mainly driven by falling prices for precious metals. The other big change was the sharp growth in the exposure of EV metals, which increased from 20% to 26% over 12 months. It is important to note that Lynas, Pilbara, Orocobre and IGO were all part of this group in September 2020 but had moved into the top 100 by September 2021. Therefore, the value of companies comprising the EV metals sector grew significantly more than the amount shown in the second chart. This means over the last 12 months the majority of growth in Resources & Energy stocks outside the top 100 was generated by stocks exposed to EV metals.

Differences in the compositional mix of ASX-listed Resources & Energy companies from 30 September 2020 to 30 September 2021. Sectors are grouped according to the principal source of revenue (or value) and are based on market capitalisation.

Uranium was another commodity to grow strongly over the last 12 months. While the energy sector grew as oil gas and coal prices rebounded from their COVID-induced lows from mid-2020, uranium stocks experienced a particularly strong rebound. We include uranium among the clean energy commodities because many North American, European and Asian countries need to maintain, or possibly expand, their nuclear power base to meet emissions targets. No uranium-focussed stocks have entered the top-100, but if consolidation was to occur in this sector, then further disruption of the commodity mix is possible.

So, is this the end of a short and sharp disruption of the Resources & Energy sectors or only the beginning? At Acorn Capital we think it is only the beginning and that this major disruption has many years left to run. Moreover, we believe this data validates our strategy of targeting Resource & Energy companies outside the top 100 on the ASX but with market caps >$10m: this is the investment universe where growth is focussed rather than the household names of old. Investors should also note that identifying the best opportunities among the 625 small- and mid-cap companies in this universe requires deep technical and financial skills that very few fund managers possess. Acorn Capital we have 20 years of sector learnings and institutional memory in exactly the right part of the Resources & Energy sectors where the growth is occurring. Those investing in the NextGen Resources Fund are not only targeting an exciting part of the market but are utilising a team with the knowledge and experience to extract the best value.